So far so good. These words are probably a fair assessment of Europe’s progress thus far in its struggle against inflation. Policy interest rates have been raised resolutely, central banks have signaled commitment to keeping them high for as long as necessary, and inflation is down sharply from the double-digit highs of last year.

Underlying inflation, however, is proving more stubborn than headline inflation, which includes energy, food, and other more volatile items. Bringing it back to target, durably, remains a matter of urgency. Entrenched high inflation is distortionary. Moreover, prolonged inflation means prolonged high real interest rates, which would hurt private and public investment and therefore future growth.

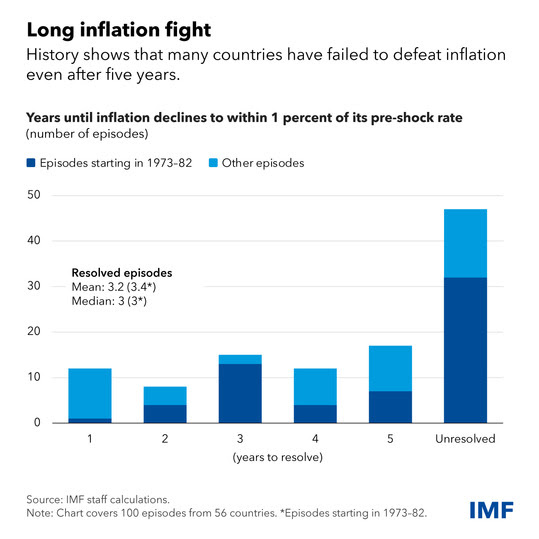

Yet, as we show in a recent paper that looks at 100 inflation episodes worldwide, history is littered with examples of premature celebrations of victory in disinflationary fights—each time with inflation making a comeback.

This is a costly mistake that Europe can and must avoid. Price stability needs to be re-established in the first attempt. And as the effects of tighter monetary policies begin to be felt across Europe, and as criticism inevitably mounts, central banks must not blink. Fiscal policymakers can and should help by lowering still-high deficits to rebuild or preserve fiscal buffers, which will help bring inflation down faster.

In our projections, we see inflation returning to target sometime in 2025. Before then, nominal wage growth will pick up, recouping some of labor’s lost real income. With tight policies softening domestic demand, firms’ profit margins should compress and help mitigate the impact of faster wage growth on inflation, as we explain in recent research.

There are, of course, risks around our central scenario. Wage growth might outpace our assumptions, driving up labor costs. Profit margins might stay high. And, as the recent spike in oil prices shows, commodity price shocks remain a concern. On the other side of the ledger, if interest-rate increases transmit faster than we anticipate, or more strongly, to demand and to inflation expectations, inflation could decline more rapidly.

Monetary policy should remain data dependent. Under the baseline, this means it should stay the course and remain restrictive in most countries. If inflation comes in much lower or higher, rates would have to adjust. But, in general, during a disinflation effort, it is better to err on the side of doing a little bit more than of doing less in response to an upside surprise.

A time for interest rate cuts will eventually come. When it does, it is best that such cuts do not involve reversals. That time is not now. Urgency also requires patience.